Why We’re Still Open For Business At Asymmetric

By now, we’re assuming you’ve heard from tech pundits of all stripes that

We’re thrilled to share that Asymmetric Capital Partners has closed Asymmetric Fund II at $137 million in capital commitments, exceeding our $125 million target. Fund II is comprised of return investors from our top ranking Fund I, joined by a strong group of new family office and institutional LPs who share our conviction in the Asymmetric approach.

The fund was covered in this morning's Fortune Term Sheet.

When we launched in 2021, our goal was simple: to be the most thoughtful and conviction-driven partner to early-stage founders. With Fund I ($105M), we backed 29 core investments and have already seen three strong exits, including Torc (acquired by Randstad), EvolutionIQ (acquired by CCC Intelligent Solutions), and Zorus (acquired by DNSFilter). Fund I ranks in the top 5% of its vintage1, validating our disciplined, operator-centric model.

Just 8% of 2021-vintage first-time funds have raised a successor vehicle2, making Fund II an especially meaningful milestone in what has been a historically difficult fundraising environment.

With Fund II, we’ve doubled down on the strategy that made Fund I successful with even greater concentration and conviction. The fund will target 20% ownership in companies where a single outcome has the potential to return the fund.

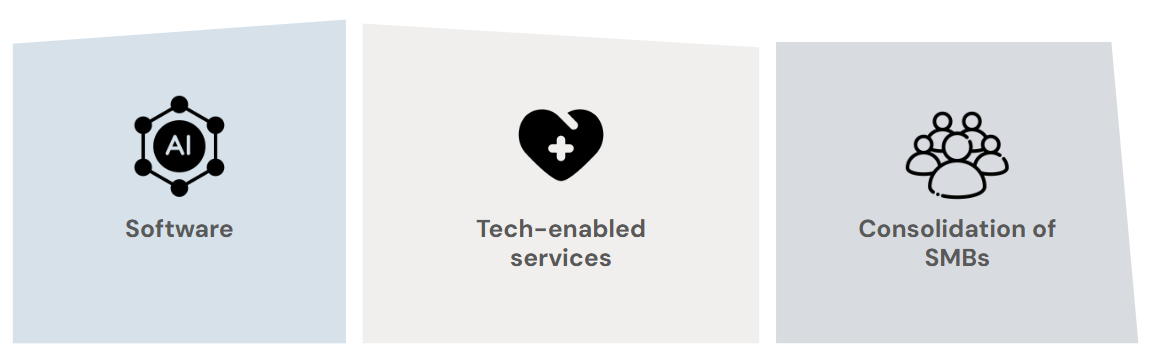

Our investment focus remains consistent across three core areas where our team brings deep operational and strategic expertise:

Fund II investments will typically range from $2–10 million as a lead in Pre-seed through Series A rounds, enabling us to partner with founders early, when thoughtful support matters most.

At Asymmetric, our DNA is different by design. Our team combines deep investing experience with real-world operating expertise.

As former PE investors, we’ve led transactions that required rigorous diligence, thoughtful structuring, and an unwavering focus on unit economics. As operators, we’ve been in the trenches building and scaling businesses; scrambling to make payroll, refining go-to-market strategies, and navigating the messy realities that early-stage founders face.

This blend of perspectives is core to Asymmetric’s approach. It allows us to engage with founders as true partners, not just capital providers. At times that means refining an idea pre-launch, recruiting key executives, or advising on an acquisition strategy. Fund II is designed to apply this unique mix of skills in a more concentrated way, enabling us to take meaningful ownership stakes and help shape the trajectory of the companies we back.

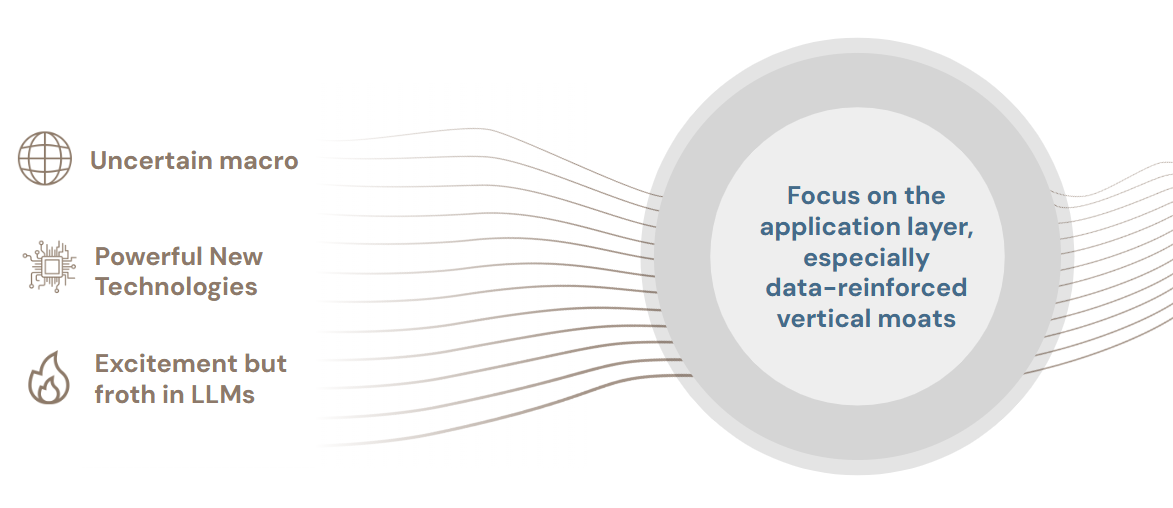

We believe the current environment is one of the most compelling moments in recent memory to be investing at the earliest stages.

Yes, the macro backdrop has been volatile. But history shows that turbulence often breeds transformation. Stripe, Uber, Airbnb, and many of today’s defining technology companies were born in uncertain times. We see today as no different: while some opportunities are weakened, others are strengthened — from the rise of modern, tech-enabled manufacturing to the acceleration of AI-driven tools and IoT-enabled systems reshaping entire industries.

The enthusiasm around AI has created both opportunity and froth. Mega-funds, with their need to deploy vast amounts of capital, are often confined to the broadest markets and most capital-consumptive models. That leaves a gap — one we are eager to fill — for nimble, capital-efficient businesses that leverage enabling technologies like AI without relying on massive burn or speculative valuations.

We see AI not as an end in itself, but as an enabling layer. Our portfolio companies are positioned to benefit from AI adoption regardless of which foundational models win. By focusing on vertical software players who can aggregate proprietary industry data, we help build durable moats that are defensible no matter how the AI infrastructure layer evolves.

Finally, attractive sub-sectors that once attracted intense venture competition have now seen capital retreat. We believe this creates fertile ground for disciplined investors with a long-term view. For us, the opportunity lies in backing founders with sensible unit economics, sector-specific expertise, and the ability to turn disruption into durable industry leadership.

The net effect: the early-stage landscape is ripe with opportunity, and Fund II is structured to seize it.

Our investor base continues to be composed entirely of value-added LPs: founders, family offices, and operators with direct experience scaling technology businesses. The Asymmetric GP team has also made a significant personal capital commitment to Fund II, underscoring alignment with our partners.

A meaningful share of our deal flow comes directly from founder referrals. As one founder recently shared:

"What sets Asymmetric apart is how deeply they commit. They understood our vision right away and have supported us across every front — recruitment, strategy, and fundraising. They’ve been true partners, always stepping in with the right support at the right time.” — Muthu Alagappan, Founder & CEO of Counsel Health

With Fund II, we’re excited to continue our mission of being true thought partners to the next generation of exceptional founders. We remain committed to disciplined, high-conviction investing and to the belief that when operators, investors, and founders work shoulder-to-shoulder, extraordinary companies get built.

1 Fund performance DPI metrics as of June 30, 2025. Benchmarking based on Cambridge Associates US Venture Capital: Fund Since Inception Analysis for 2021 vintage year funds as of June 30, 2025.

2 Pitchbook 2021 vintage first time venture capital fund data.